At the risk of over-simplifying, the difference between “supply-side economics” and “demand-side economics” is that the former is based on microeconomics (incentives, price theory) while the latter is based on macroeconomics (aggregate demand, Keynesianism).

When discussing the incentive-driven supply-side approach, I often focus on two key points.

- Marginal tax rates matter more than average tax rates because the incentive to earn additional income (rather then enjoying leisure)

is determined by whether the government grabs a small, medium, or large share of any extra earnings.

is determined by whether the government grabs a small, medium, or large share of any extra earnings. - Some taxpayers such as investors, entrepreneurs, and business owners are especially sensitive to changes in marginal tax rates because they have considerable control over the timing, level, and composition of their income.

Today, let’s review some new research from Spain’s central bank confirms these supply-side insights.

Here’s what the authors investigated.

The impact of personal income taxes on the economic decisions of individuals is a key empirical question with important implications for the optimal design of tax policy. …the modern public finance literature has devoted significant efforts to study behavioral responsesto changes in taxes on reported taxable income… Most of this work focuses on the elasticity of taxable income (ETI), which captures a broad set of real and reporting behavioral responses to taxation. Indeed, reported taxable income reflects not only individuals’ decisions on hours worked, but also work effort and career choices as well as the results of investment and entrepreneurship activities. Besides these real responses, the ETI also captures tax evasion and avoidance decisions of individuals to reduce their tax bill.

By the way, “elasticity” is econ-speak for sensitivity. In other words, if there’s high elasticity, it means taxpayers are very responsive to a change in tax rates.

Anyhow, here’s how authors designed their study.

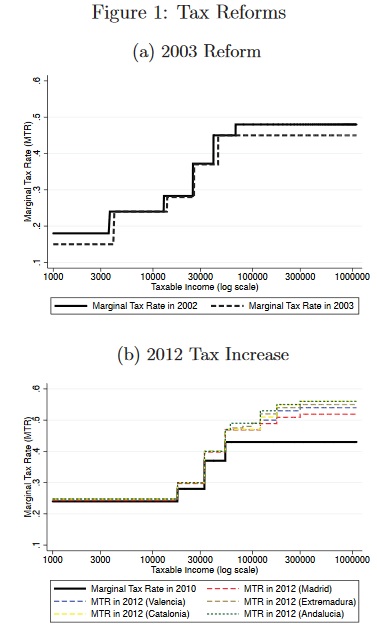

In this paper, we estimate the elasticity of taxable income in Spain, an interesting country to study because during the last two decades it has implemented several major personal income tax reforms… In the empirical analysis, we use an administrative panel dataset of income tax returns… We calculate the MTR as a weighted average of the MTR applicable to each income source (labor, financial capital, real-estate capital, business income and capital gains).

You can see in Figure 1 that the 2003 reform was good for taxpayers and the 2012 reform was bad for taxpayers.

If nothing else, though, these changes created the opportunity for scholars to measure how taxpayers respond.

And here are the results.

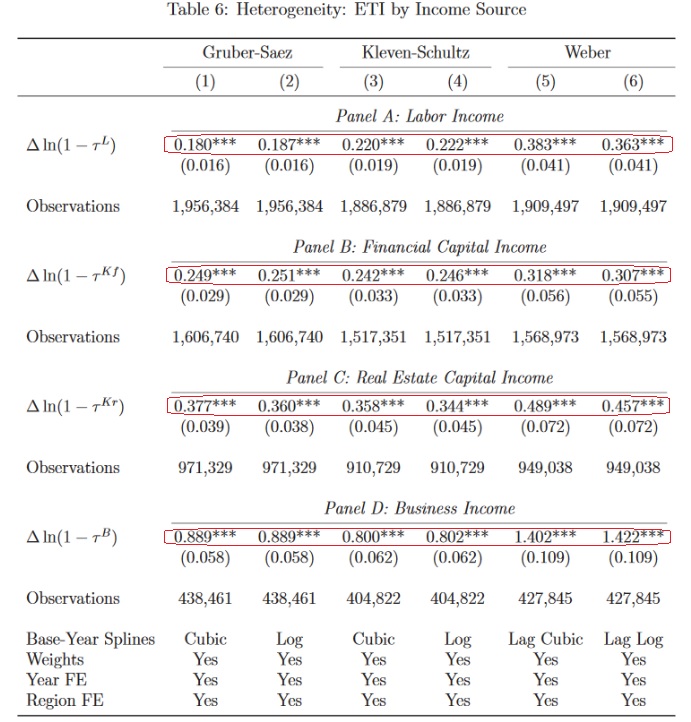

We obtain estimates of the ETI around 0.35 using the Gruberand Saez (2002) estimation method, 0.54 using Kleven and Schultz (2014)’s method and 0.64 using Weber (2014)’s method. …In addition to the average estimates of the ETI, we analyze heterogeneous responses across groups of taxpayers and sources of income. …As expected, stronger responses are documented for groups of taxpayers with higher ability to respond. In particular, self-employed taxpayers have a higher ETI than wage employees, while real-estate capital and business income respond more strongly than labor income. …we find large responses on the tax deductions margin, especially private pension contributions.

In other words, taxpayers do respond to changes in tax policy.

And some taxpayers are very sensitive (high elasticity) to those changes.

Here’s Table 6 from the study. Much of it will be incomprehensible if you’re not familiar with econometrics. But all that matters is that I circled (in red) the measures of how elasticities vary based on the type of income (larger numbers mean more sensitive).

I’ll close with a very relevant observation about American fiscal policy.

Currently, upper-income taxpayers finance the vast majority of America’s medium-sized welfare state.

But what if the United States had a large-sized welfare state, like the ones that burden many European nations?

If you review the data, those large-sized welfare states are financed with stifling tax burdens on lower-income and middle-class taxpayers. Politicians in Europe learned that they couldn’t squeeze enough money out of the rich (in large part because of high elasticities).

Indeed, I wrote early this year about how taxes are confiscating the lion’s share of the income earned by ordinary workers in Spain.

And if we adopt the expanded welfare state envisioned by Bernie Sanders, Alexandria Ocasio-Cortez, and Kamala Harris, the same thing will happen to American workers.

P.S. I admire how Spanish taxpayers have figured out ways of escaping the tax net.

P.P.S. There’s also evidence about the impact of Spain’s corporate tax.

No comments:

Post a Comment